Secured Lending

Understanding Secured Lending

Secured lending represents a fundamental approach to mitigating credit risk in financial services. At its core, secured lending is a financial arrangement where a borrower pledges specific assets as collateral, providing the lender with a safety net in case of default. These assets—from real estate and equipment to accounts receivable and securities—are critical risk management tools.

Collateral as a First-Class Citizen

In modern lending, secured credit represents far more than a simple relationship between loan balances and asset values. Yet many loan management systems treat collateral as an afterthought—a static field to be updated occasionally, disconnected from the dynamic reality of lending operations.

Canopy fundamentally reimagines this approach by treating collateral as a first-class citizen in our lending ecosystem. This means collateral isn't just a value stored alongside a loan—it's an active participant in your lending operations, driving workflows, influencing decisions, and evolving with market conditions.

Consider how this transforms secured lending: When a borrower pledges securities as collateral, our system doesn't simply record their value and wait for manual updates. Instead, it maintains an ongoing awareness of that collateral's worth, automatically adjusting credit availability, triggering protective actions when values decline, and providing real-time insight into your risk position. This dynamic relationship between collateral and loan servicing means your lending operations can respond to market changes as they happen, not after the fact.

This elevation of collateral to first-class status ripples throughout our entire platform. From automated valuation updates to comprehensive risk management workflows, from portfolio-wide analytics to borrower-level collateral positions—every feature is built with the understanding that collateral is not a passive security measure but an active component of modern lending operations. The result is a system that doesn't just track collateral—it empowers you to make collateral work harder for your lending program.

The Collateral Landscape

Not all collateral is created equal. Our system recognizes the nuanced world of asset-backed lending, supporting a diverse range of collateral types:

Real estate might represent a traditional, stable form of collateral with values that change slowly. In contrast, accounts receivable or cryptocurrency present a more dynamic collateral environment, with values that can fluctuate rapidly. Our platform is designed to handle this complexity, providing lenders with flexible tools to manage diverse asset types.

Supported asset typesReal estate, vehicles, equipment, accounts receivables, inventory, business assets, securities, cash, cryptocurrency, collectibles

More information on each can be found in our collateral APIs

Loan-to-Value: The Critical Metric

The Loan-to-Value (LTV) ratio is the cornerstone of secured lending risk management. This metric represents the relationship between the loan amount and the value of the underlying collateral. For instance, a $750,000 loan secured by a $1,000,000 property would have a 75% LTV ratio.

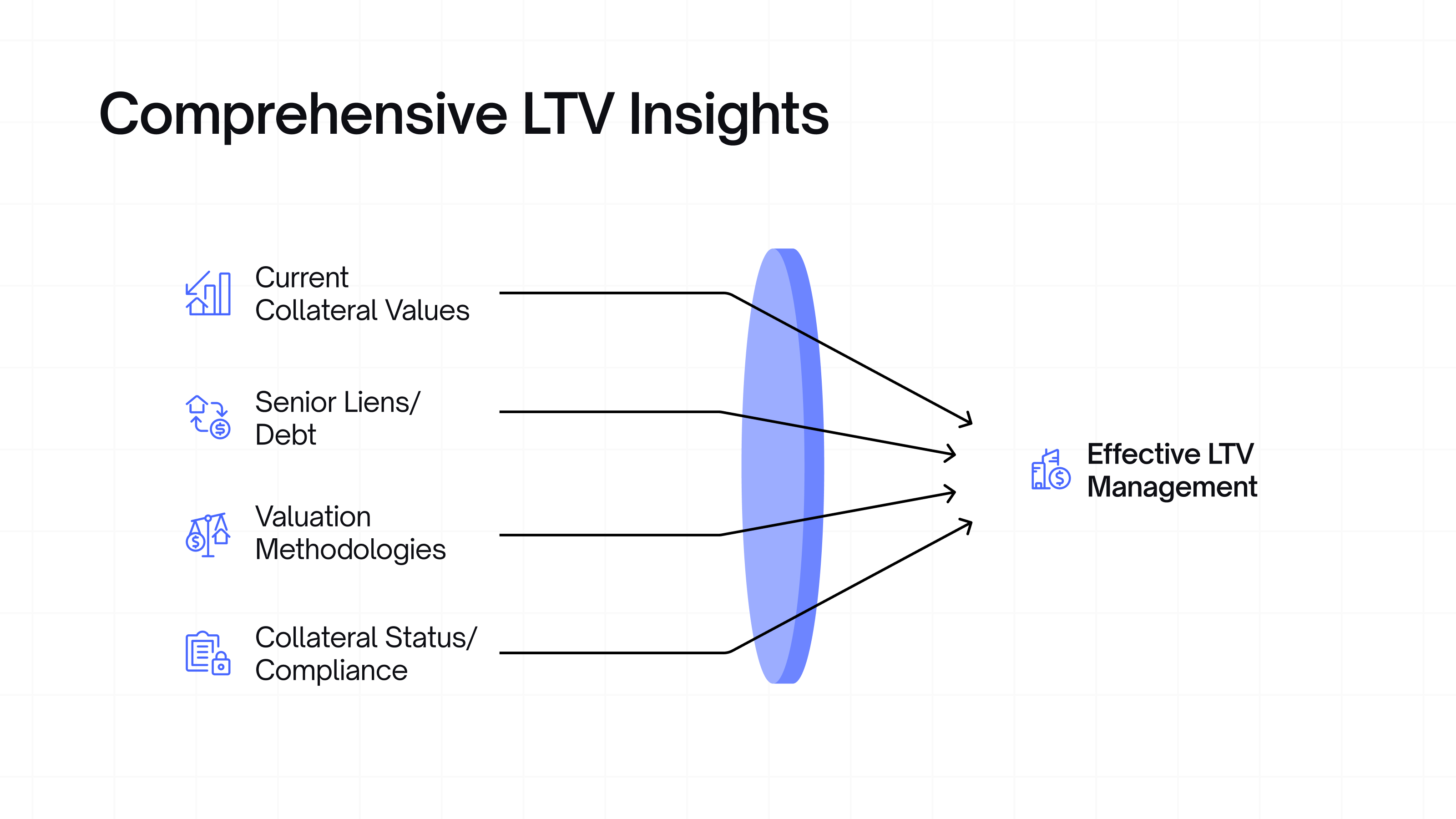

Don't just track LTV; instead, let Canopy provide you with comprehensive insights into it.

Updated about 1 year ago

What’s Next

Secured lending is evolving. Our platform is designed to grow with emerging asset classes, valuation methodologies, lien information and risk mitigation approaches. Please explore what Canopy has to offer